In recent weeks, two insurers with significant legacies of occurrence-based general liability coverage took important steps to liquidate their estates.

In recent weeks, two insurers with significant legacies of occurrence-based general liability coverage took important steps to liquidate their estates.

Bedivere Insurance Company (OneBeacon) Liquidation

The first insurers are associated with Bedivere Insurance Company, formerly known as OneBeacon Insurance Company (OBIC). OBIC’s history stretches back to the 1800s but is most well known as the successor to the General Accident and Commercial Union families of insurers. These companies wrote many policies from the 1960s through the 2000s and include Commercial Union Assurance Company, Employers Commercial Union Insurance Company, Employers’ Surplus Lines Insurance Company, Employers’ Liability Assurance Corporation Limited, General Accident Insurance Company, and CGU Insurance Company (and many other smaller companies). OBIC stopped writing new business in 2010 and entered run-off, paying claims from its historic exposures. In 2014, OneBeacon Group, OBIC’s parent, sold its run-off business to a Bermuda entity called Armour Group. The transaction included OBIC and other subsidiaries (Potomac Insurance Company, OneBeacon America Insurance Company, and The Employers Fire Insurance Company). OBIC changed its name to Bedivere Insurance Company in 2015, and in October 2020, absorbed its subsidiaries by merger.

Continue Reading ›

Temperatures in Arizona this week reached over 110 degrees Fahrenheit. The water temperature in the Florida Keys was reported to reach sauna-like levels, threatening the life of habitat-sustaining coral. Atmospheric conditions are routinely blamed for violent storms and for wildfires that darken the skies.

Temperatures in Arizona this week reached over 110 degrees Fahrenheit. The water temperature in the Florida Keys was reported to reach sauna-like levels, threatening the life of habitat-sustaining coral. Atmospheric conditions are routinely blamed for violent storms and for wildfires that darken the skies.

Early in 2021, we wrote about potential insurance implications that could arise from the then-new

Early in 2021, we wrote about potential insurance implications that could arise from the then-new  In August, we provided an

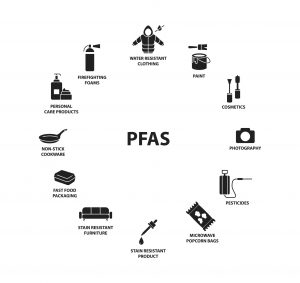

In August, we provided an  A key component of a company’s risk management function is to keep a close eye on new and developing sources of liability and to put in place appropriate insurance to respond in the event those liabilities ripen. In recent years, there has been a significant increase in legal and regulatory attention on per- and polyfluoroalkyl substances, more commonly known as “PFAS” or “forever chemicals.” PFAS are used in countless applications, and many companies across the country bear potential liability, from chemical companies to manufacturers to retailers to corporate end users. PFAS-related enforcement is focused on remedying impacts to both the environment and human health. Importantly, a company’s liability for PFAS-related contamination or bodily injury may be covered under historic general liability policies and/or modern-day pollution liability policies. As regulation and litigation relating to these ubiquitous substances continues to surge, corporate policyholders with potential exposure should be proactive to examine their insurance portfolios and position themselves for potential insurance coverage in the event they become a PFAS liability target.

A key component of a company’s risk management function is to keep a close eye on new and developing sources of liability and to put in place appropriate insurance to respond in the event those liabilities ripen. In recent years, there has been a significant increase in legal and regulatory attention on per- and polyfluoroalkyl substances, more commonly known as “PFAS” or “forever chemicals.” PFAS are used in countless applications, and many companies across the country bear potential liability, from chemical companies to manufacturers to retailers to corporate end users. PFAS-related enforcement is focused on remedying impacts to both the environment and human health. Importantly, a company’s liability for PFAS-related contamination or bodily injury may be covered under historic general liability policies and/or modern-day pollution liability policies. As regulation and litigation relating to these ubiquitous substances continues to surge, corporate policyholders with potential exposure should be proactive to examine their insurance portfolios and position themselves for potential insurance coverage in the event they become a PFAS liability target. The Biden administration has hit the ground running with executive orders, regulatory and legislative priorities, and cabinet-level and other top posts being announced on a daily basis. Our public policy colleagues have been closely tracking many of the policy priorities of the new administration and

The Biden administration has hit the ground running with executive orders, regulatory and legislative priorities, and cabinet-level and other top posts being announced on a daily basis. Our public policy colleagues have been closely tracking many of the policy priorities of the new administration and  In recent years, Wisconsin generally has been a pro-policyholder jurisdiction when it comes to long-tail environmental coverage cases. That trend continues with a decision by a Wisconsin appellate court in a case involving coverage for environmental cleanup costs at a former manufactured gas plant site. In

In recent years, Wisconsin generally has been a pro-policyholder jurisdiction when it comes to long-tail environmental coverage cases. That trend continues with a decision by a Wisconsin appellate court in a case involving coverage for environmental cleanup costs at a former manufactured gas plant site. In  Insurers have recently argued that environmental property damage claims for “closure” costs arising out of historic pollution are not covered, because the claimed damages are just “ordinary costs of doing business.” Policyholders should strongly resist denials based on this argument, which is unsupported custom and practice in the insurance industry and contradicts the terms of standard-form third-party liability policies, applicable environmental laws, and insurance law in nearly all jurisdictions.

Insurers have recently argued that environmental property damage claims for “closure” costs arising out of historic pollution are not covered, because the claimed damages are just “ordinary costs of doing business.” Policyholders should strongly resist denials based on this argument, which is unsupported custom and practice in the insurance industry and contradicts the terms of standard-form third-party liability policies, applicable environmental laws, and insurance law in nearly all jurisdictions.